Ethereum Boom Or Bust? Daniel Yan Sounds Alarm On SBET

Daniel Yan, the founder and CIO of Kryptanium Capital, a managing partner at Matrixport Ventures, and previously an executive at Bitmain and Merrill Lynch, writes today via X: “Everyone is comparing SBET to MSTR and thus concludes super-bullishly for both ETH and SBET. Together with the ETF massive flow, the logic seems impeccable… I think SBET differs massively from MSTR on two fronts… All the above point to a maximization of short-term interest.”

The comparison of SharpLink Gaming (SBET) to MicroStrategy (MSTR) has become a fixture of crypto-equity chatter as Ether rallies to 16-month highs on the back of record US spot-ETF inflows. But in a post published this morning, venture investor Daniel Yan argues that the two “proxy” trades share less DNA than the market assumes.

SBET Isn’t MicroStrategy—What It Means For Ethereum Price

SharpLink’s metamorphosis from an i-gaming software vendor into the world’s largest corporate Ether holder has been dizzyingly fast. Since the firm announced its treasury pivot on 2 June, it has amassed 280,706 ETH (≈ $925 million) and staked nearly all of it, earning 415 ETH in rewards. To fund the spree, SharpLink sold 24.6 million shares for $413 million via an at-the-market (ATM) facility between 7 and 11 July. The company still has $257 million of authorised capital it has yet to commit to the market.

Management insists dilution is offset by growing “ETH Concentration” (ETH ÷ 1,000 assumed diluted shares), which has risen from 2.00 to 2.46 ETH in just five weeks. Nevertheless, Yan warns that the very mechanism powering SharpLink’s accumulation—constant equity issuance—is also a pressure point: “This method creates a massive dilution effect on the ETH-per-share metric, which makes SBET price more vulnerable to negative shocks.”

MicroStrategy’s Bitcoin strategy is held together by cheap, long-dated leverage. Since mid-2020 the firm has floated $8.2 billion of convertible notes—all funnelled into BTC—and only secondarily tapped its own ATM shelf. Because converts embed an equity option, they dilute only if MSTR’s share price leaps, effectively synchronising new issuance with bullish sentiment. Yan calls this a “flywheel” that SBET lacks.

Indeed, five of MicroStrategy’s six convert issues are already deep in the money as MSTR flirts with all-time highs, turning the debt into quasi-equity on highly favourable terms. By contrast, SharpLink relies almost exclusively on equity sales; every fresh tranche increases the denominator immediately, regardless of where SBET trades.

Yan also highlights governance asymmetry: SharpLink was recapitalised by “one of the largest consortium of ETH holders,” whose own SBET shares unlock in roughly five months. He frames the arrangement as a “multi-party prisoner’s dilemma,” implying insiders may be incentivised to monetise quickly rather than steward a decades-long treasury strategy.

No comparable unlocking event hangs over MicroStrategy, whose executive chairman Michael Saylor owns the bulk of the voting stock and has repeatedly pledged never to sell.

Yan’s comments land just as Ether ETFs smash records. US spot funds absorbed $726.6 million in net inflows on Wednesday, their best day since launch, lifting cumulative holdings above 5 million ETH. Bulls argue that such flows will continue to buoy both Ether and any equity that warehouses it.

Even Yan concedes “there is merit in this for the short term.” But his analysis underscores that the path-dependency of SharpLink’s model—equity issuance first, crypto purchases later—carries different risks from MicroStrategy’s debt-driven lever. The key divergence is simple: MicroStrategy’s converts dilute only if the bet is already winning; SharpLink’s ATM dilutes so the bet can be placed.

Yan is not forecasting an imminent crash—he explicitly disavows any short position in Ether—but he urges investors caught up in “the euphoric period” to scrutinise capital-structure mechanics. If SharpLink’s insiders do treat the company as a short-term vehicle and ETF momentum cools, the ATM-powered “flywheel” could spin the opposite way: more shares, lower ETH-per-share, weaker SBET.

Conversely, if Ether keeps climbing and the firm times its issuance astutely, shareholders could still enjoy MicroStrategy-style convexity. The difference, as Yan makes clear, is that SharpLink’s leverage is worn on the cap table, not tucked inside a convertible note.

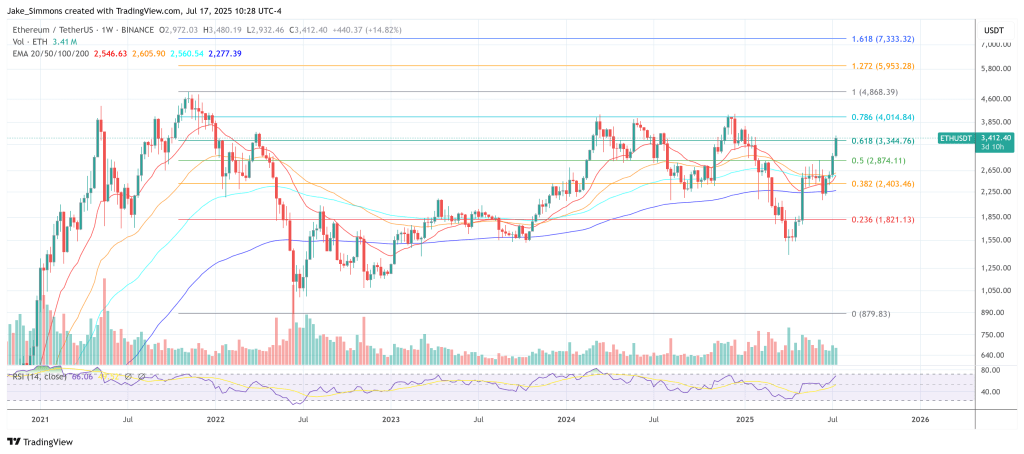

At press time, ETH traded at $3,412.

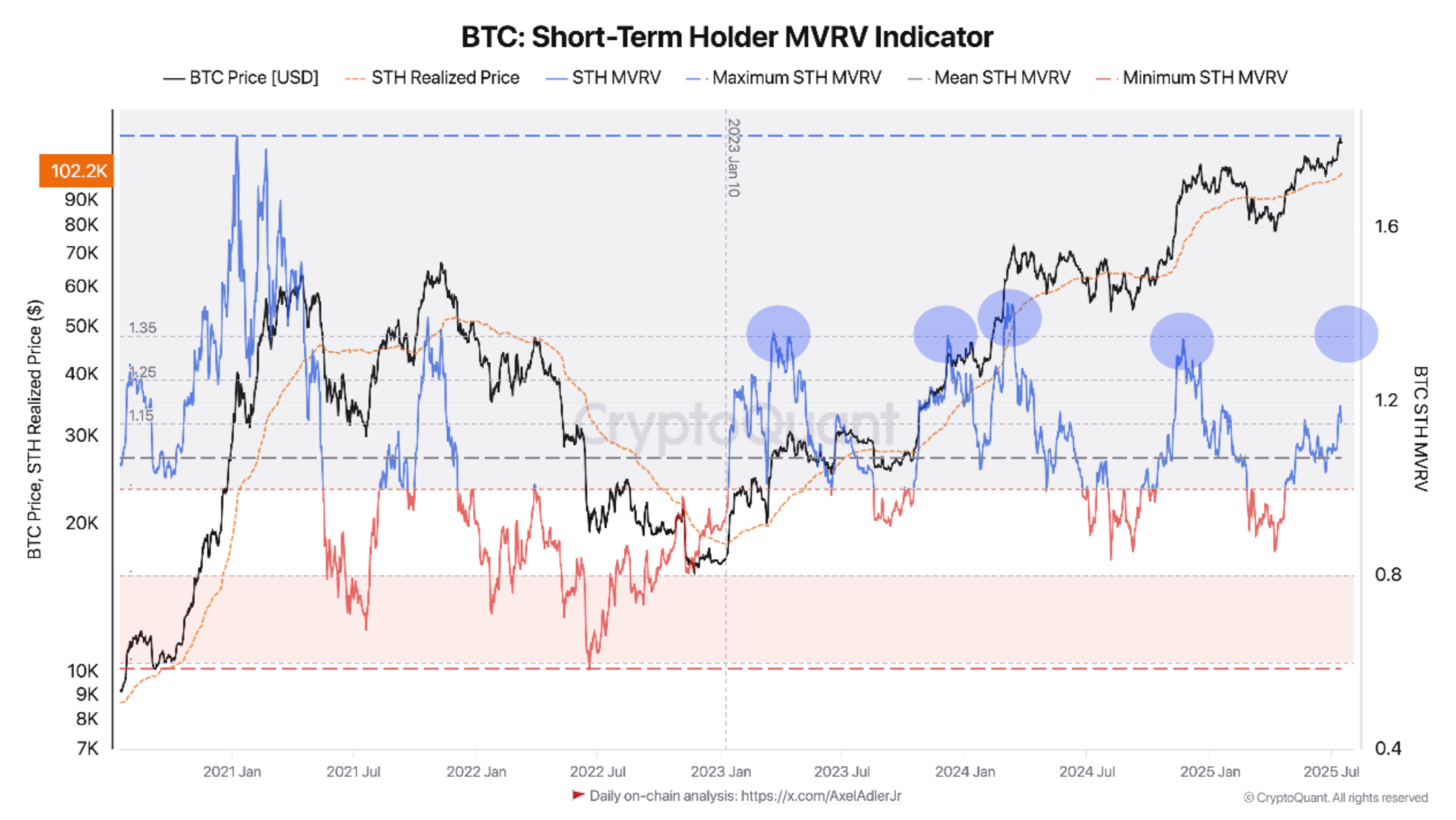

Bitcoin Rally Not Over Yet? Short-Term Holder MVRV Suggests Further Upside

As Bitcoin (BTC) consolidates just below the $120,000 mark, concerns are mounting over whether the t...

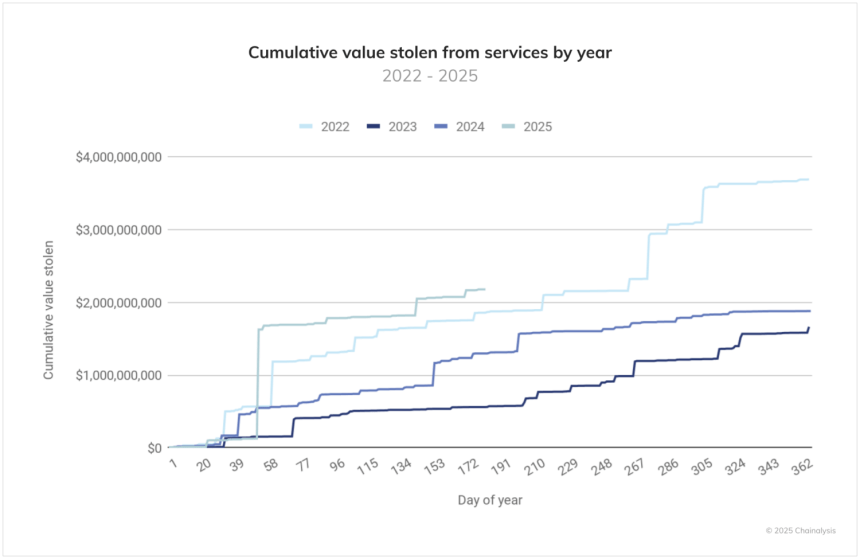

2025 Crypto Thefts Spike: Stolen Funds Hit $2.7 Billion In H1– Report

As the market soars with bullish momentum, crypto theft has also seen a record-breaking performance ...

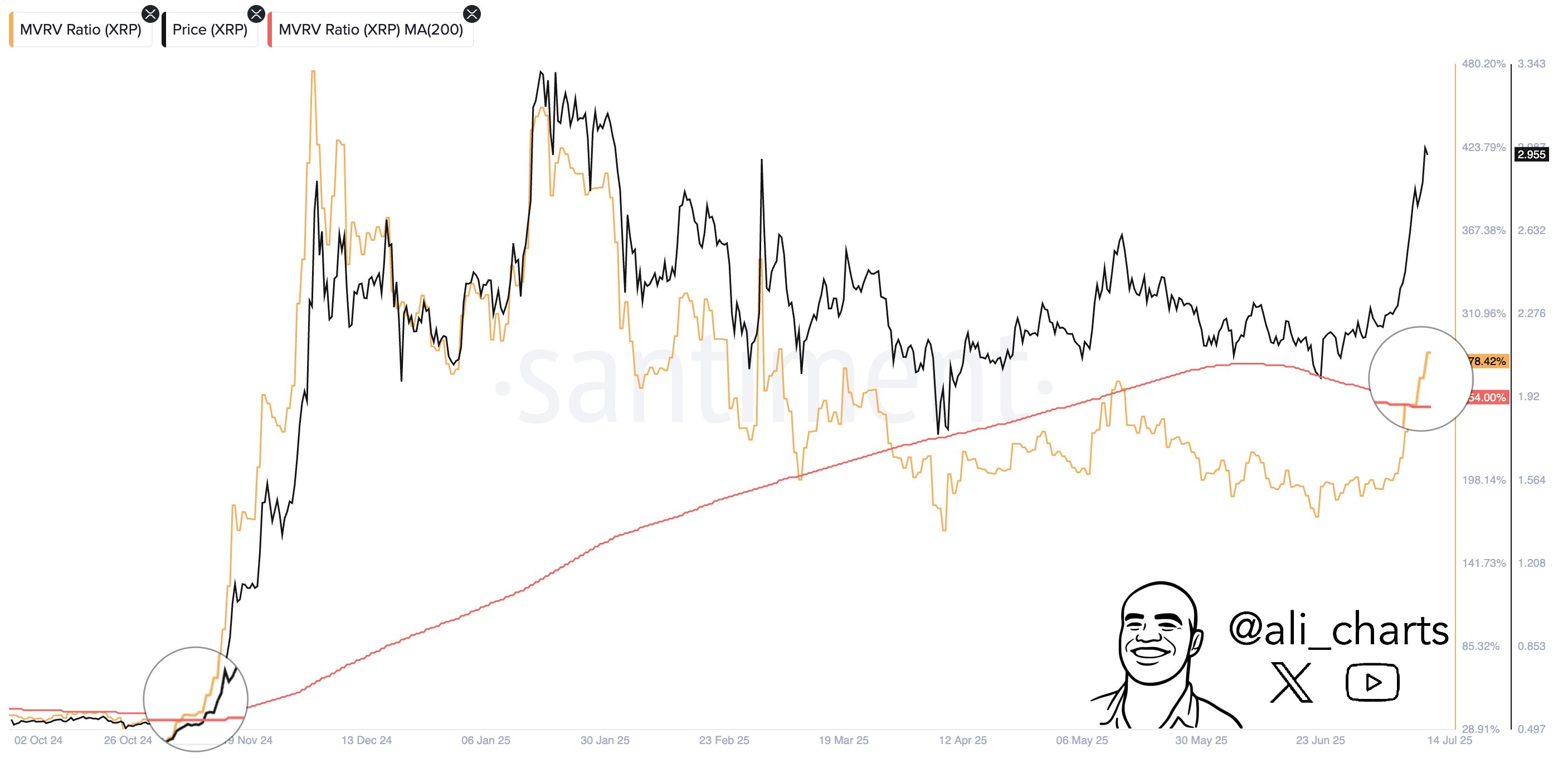

XRP MVRV Ratio Flashes Signal That Last Led To 630% Surge

An analyst has pointed out that the XRP Market Value to Realized Value (MVRV) Ratio has just formed ...